Home

/ How To Calculate Covariance Matrix - Covarianceis a measure of the extent to which corresponding elements from two sets of ordered data move in the same direction.

How To Calculate Covariance Matrix - Covarianceis a measure of the extent to which corresponding elements from two sets of ordered data move in the same direction.

How To Calculate Covariance Matrix - Covarianceis a measure of the extent to which corresponding elements from two sets of ordered data move in the same direction.. What are the properties of variance? See full list on stattrek.com , xnk x is an n x k matrix of raw scores: = raw score in the first set of scores. See full list on stattrek.com

Mathematically, it is the average squared deviation from the mean score. Transform the raw scores from matrix x into deviation scores for matrix x. We use the following formula to compute population covariance. X y z x 11.50 50.00 34.75 y 50.00 1250.00 205.00 z 34.75 205.00 110.00 the 11.50 is the variance of x, 1250.0 is the variance of y, and 110.0 is the variance of z. For variance, in words, subtract each value from the dimension mean.

Using the Variance Covariance matrix to calculate the ... from i.ytimg.com We use the following formula to compute population variance. What are the properties of variance? Transform the raw scores from matrix x into deviation scores for matrix x. 1 calculation of covariance matrix from data matrix suppose we have a data matrix with rows corresponding to subjects and columns corresponding to variables. Covariance matrix for sample data matrix. For variance, in words, subtract each value from the dimension mean. Is a covariance matrix always square? = raw score in the first set of scores.

See full list on stattrek.com

Compute x'x, the k x k deviation sums of squares and cross products matrix for x. See full list on stattrek.com = deviation score in the first set of scores. The covariance matrix definition the covariation of data thecovariance matrixrefers to the symmetric array of numbers s = 0 b b b b b @ s2 1 s12 s13 s1p s21 s2 2 s23 s2p s31 s32 s2 3 s3p. Nov 03, 2017 · the covariance matrix for this data set is: Transform the raw scores from matrix x into deviation scores for matrix x. For variance, in words, subtract each value from the dimension mean. Xi is the ith raw score in the set of scores xi is the ith deviation score in the set of scores var(x) is the variance of all the scores in the set See full list on stattrek.com What are the properties of variance? We can calculate a mean for each variable and replace the data matrix with a matrix of 1 calculation of covariance matrix from data matrix suppose we have a data matrix with rows corresponding to subjects and columns corresponding to variables. Covariance matrix for sample data matrix.

See full list on stattrek.com Covariance matrix • representing covariance between dimensions as a matrix e.g. Varianceis a measure of the variability or spread in a set of data. Suppose x is an n x k matrix holding ordered sets of raw data. Covariance matrix for sample data matrix.

Covariance analyses. (a) Covariance matrix computed from ... from www.researchgate.net For variance, in words, subtract each value from the dimension mean. X y z x 11.50 50.00 34.75 y 50.00 1250.00 205.00 z 34.75 205.00 110.00 the 11.50 is the variance of x, 1250.0 is the variance of y, and 110.0 is the variance of z. See full list on stattrek.com The covariance matrix definition the covariation of data thecovariance matrixrefers to the symmetric array of numbers s = 0 b b b b b @ s2 1 s12 s13 s1p s21 s2 2 s23 s2p s31 s32 s2 3 s3p. = deviation score in the first set of scores. We use the following formula to compute population covariance. Varianceis a measure of the variability or spread in a set of data. = raw score in the first set of scores.

Mathematically, it is the average squared deviation from the mean score.

For variance, in words, subtract each value from the dimension mean. Mathematically, it is the average squared deviation from the mean score. Transform the raw scores from matrix x into deviation scores for matrix x. We use the following formula to compute population variance. Covariance matrix for sample data matrix. Xi is the ith raw score in the set of scores xi is the ith deviation score in the set of scores var(x) is the variance of all the scores in the set = raw score in the first set of scores. We can calculate a mean for each variable and replace the data matrix with a matrix of See full list on stattrek.com = deviation score in the first set of scores. The covariance matrix definition the covariation of data thecovariance matrixrefers to the symmetric array of numbers s = 0 b b b b b @ s2 1 s12 s13 s1p s21 s2 2 s23 s2p s31 s32 s2 3 s3p. Suppose x is an n x k matrix holding ordered sets of raw data. See full list on stattrek.com

For variance, in words, subtract each value from the dimension mean. 1 calculation of covariance matrix from data matrix suppose we have a data matrix with rows corresponding to subjects and columns corresponding to variables. Mathematically, it is the average squared deviation from the mean score. X y z x 11.50 50.00 34.75 y 50.00 1250.00 205.00 z 34.75 205.00 110.00 the 11.50 is the variance of x, 1250.0 is the variance of y, and 110.0 is the variance of z. Compute x'x, the k x k deviation sums of squares and cross products matrix for x.

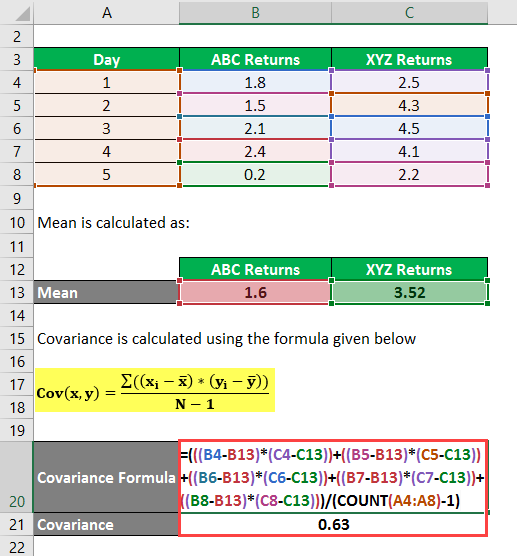

Covariance Formula | Examples | How To Calculate Correlation? from cdn.educba.com Varianceis a measure of the variability or spread in a set of data. Covariance matrix • representing covariance between dimensions as a matrix e.g. Is a covariance matrix always square? Covariance matrix for sample data matrix. Compute x'x, the k x k deviation sums of squares and cross products matrix for x. Transform the raw scores from matrix x into deviation scores for matrix x. See full list on stattrek.com We use the following formula to compute population covariance.

Compute x'x, the k x k deviation sums of squares and cross products matrix for x.

What are the properties of variance? Suppose x is an n x k matrix holding ordered sets of raw data. Where, n = number of scores in each set of data. See full list on stattrek.com Varianceis a measure of the variability or spread in a set of data. X = mean of the n scores in the first data set. We use the following formula to compute population covariance. Compute x'x, the k x k deviation sums of squares and cross products matrix for x. See full list on stattrek.com = raw score in the first set of scores. Covarianceis a measure of the extent to which corresponding elements from two sets of ordered data move in the same direction. X y z x 11.50 50.00 34.75 y 50.00 1250.00 205.00 z 34.75 205.00 110.00 the 11.50 is the variance of x, 1250.0 is the variance of y, and 110.0 is the variance of z. We use the following formula to compute population variance.